On 28 March 2025, Treasury published the much-anticipated draft determination outlining the proposed notification thresholds and forms for the new merger regime. The regime commences on a voluntary basis from 1 July 2025 and becomes compulsory on 1 January 2026.

The draft determination sets out the notification thresholds and tests that trigger a requirement to notify the ACCC of a proposed acquisition as well as the forms, information and documents that must accompany the notification.

Submissions on the draft are due on 2 May 2025, the day before the Australian federal government election.

Notification thresholds

The proposed thresholds triggering notification (outlined below) are largely as foreshadowed, with the exception that the private transaction designation that was proposed by the Treasurer, at the request of the ACCC, has not been included (all figures shown in AUD).

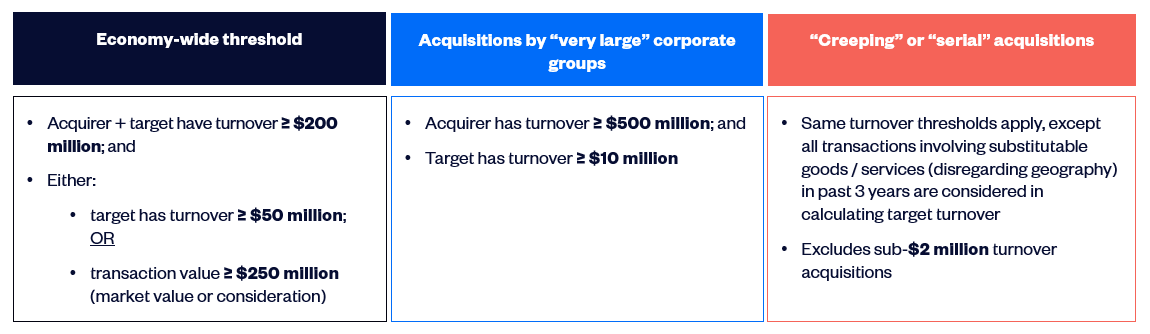

Note: For the purpose of the above thresholds, ‘acquirer’ includes all connected entities and ‘target’ includes all connected entities other than entities that are not being indirectly acquired. In all cases, the target must have a material connection to Australia. All the above figures are indexed annually. Large supermarkets must notify regardless of thresholds.

Please refer to our ‘cheat sheet’ below for a breakdown of the key elements of these proposed notification thresholds.

What this means for you

If you are considering merger or acquisition in the coming 6-12 months, you should factor in the following aspects of your transaction:

Transaction value test met if market value or consideration is $250 million or more: An acquisition will satisfy the transaction value test where the greater of the following is $250 million or more:

a. The sum of the ‘market values’ of all the shares and assets being acquired as part of the agreement explained to be the price that “a willing, but not anxious, purchaser would, as at the date in question, have had to pay to a vendor who was not unwilling, but not anxious, to sell”.

b. The ‘consideration’, explained as the amount paid for the target and includes cash and non-cash consideration.

The turnover thresholds are based on ‘current GST turnover’. The A New Tax System (Goods and Services Tax) Act 1999 defines this as the sum of the values of all the supplies that the entity made or is likely to make in the period of 12 months ending with the current month. As noted in the Explanatory Statement to the draft determination, this calculation excludes certain supplies, including input taxed supplies, supplies that are not for consideration and supplies that are not made in connection with a business or other enterprise the entity carries on.

For corporate groups and private capital, turnover of ‘connected entities’ is relevant to calculating turnover that may trigger the thresholds: Parties must consider relevant ‘connected entities’ of the merger parties. This includes:

a. ‘Associated entities’, which has a broad meaning under s 50AAA of the Corporations Act, including where (i) the relevant entity controls the second entity or (ii) has a qualifying interest in the second entity, has a significant influence over them and the interest is material to the relevant entity.

b. Entities that ‘control’ the target entities. This applies where the relevant entity and one or more of its associates jointly determine the outcome of decisions about the second entity's financial and operating policies (s 50AA of the Corporations Act as modified by s 51ABS(2) of the Competition and Consumer Act).

Large supermarkets must notify regardless of thresholds: In addition to the above thresholds, the draft determination also proposes that Coles and Woolworths and their connected entities will be required to notify the ACCC of acquisitions of supermarket businesses or land for supermarket businesses, regardless of whether those transactions meet the general notification thresholds.

Low bar for jurisdictional nexus to Australia: An acquisition that meets the turnover or transaction value thresholds will be notifiable if the target is ‘connected with Australia’, which means the target carries on, or intends to carry on, business in Australia. The Explanatory Statement states that the words ‘intends to carry on a business’ will carry their ordinary meaning. Australian courts have considered that where a company aims to and has a prospect of, making a profit, it is presumed the company intends to carry on a business. This may mean a transaction would be notifiable even where the target has no turnover in Australia but simply ‘intends to carry on business’ in Australia (that is, if the acquirer has ≥$200 million in Australian turnover and the transaction value is ≥$250 million).

Very prescriptive information requirements, even in the ‘short’ notification form: The notification forms (even the short form) have prescriptive information and significant data and documents requirements upfront, including board documents on the transaction plans and competitive conditions. The Explanatory Statement states that merger parties are required to submit the short form for acquisitions that are ‘unlikely to raise competition concerns’ and the long form for other acquisitions. The ACCC published its provisional guidance on when parties should use the long form notification based on the level of combined market share and the level of market share increment for horizontal, vertical and conglomerate mergers. This guidance also indicates merger parties should complete the long form where the transaction involves acquiring a firm that is a vigorous and effective competitor, developing significant product or controlling access to a significant input or asset. We discuss this provisional guidance further below.

New anti-avoidance provision: The draft determination contains a new anti-avoidance provision regulating efforts to circumvent notification. It carves out the “effects of a scheme if it would be reasonable to conclude that the purpose of the person, or one of the persons, who enters into or carries out the scheme or any part of the scheme is to avoid an acquisition, being an acquisition that is required to be notified”.

Still waiting for important information: We are still waiting to see several significant requirements that remain as placeholders in the draft determination, including when notification waivers can be issued, forms and requirements of appeals to the Australian Competition Tribunal and application form requirements for the substantial public benefits review phase. As the government is now in caretaker mode until the Australian federal election on 3 May 2025, we are unlikely going to receive further guidance before the regime voluntarily commences on 1 July 2025.

The proposed notification thresholds: cheat sheet

As summarised in the diagram below, parties will need to notify the ACCC of acquisitions if the acquisition involves shares or assets that are “connected with Australia” (that is where the target carries on a business or, very broadly, intends to carry on a business, in Australia) and the following tests are met (all figures shown in AUD):

Exemptions

The draft determination also sets out certain acquisitions that are exempt from notification to the ACCC:

Certain land acquisitions: residential property developments (acquisitions made for the purpose of developing residential premises) and certain commercial property acquisitions (acquisitions by businesses primarily engaged in buying, selling or leasing land, where the acquisition is for a purpose other than operating a commercial business on the land).

Acquisitions by an administrator, receiver, receiver and manager or liquidator.

Succession: acquisitions which take place pursuant solely to a testamentary disposition, intestacy or a right of survivorship under a joint tenancy.

Financial securities: acquisitions related to certain fundraising activities from the notification requirement to avoid undue disruption to capital markets.

Money lending and financial accommodation: an express exemption for the taking of security.

Nominees and other trustees: acquisition of interests in securities.

Exchange traded derivatives: acquisitions of exchange traded derivatives.

The proposed notification forms

Overview of information requirements

Both long and short form applications contemplated will involve significant front-loading, requiring more upfront work compared with current practice. On all notifiable deals, parties will need to provide:

detailed Australia-specific data on market shares, turnover and prior deals (over the last three years)

top customers and competitors

transaction and audited financial documents

details of any non-compete agreed to protect the goodwill being acquired

organisational charts, board papers and other material.

The long form application for complex deals is more involved, requiring additional detailed data and information on:

barriers to entry

theories of competitive harm

whether any of the parties have non-controlling shareholdings or cross directorships in companies that supply the same or similar products or services as other parties to the acquisition

additional questions based on whether the acquisition is horizontal, vertical or conglomerate

more documents relating to the proposed acquisition including board papers, reports, presentations, studies, market research and more within the last three years.

Should you use the short form or long form?

As mentioned above, the Explanatory Statement states that merger parties are required to submit the short form for acquisitions ‘unlikely to raise competition concerns’ and the long form for other acquisitions.

The ACCC published provisional guidance on criteria for long form notification. The table summarises the ACCC’s preliminary views on when merger parties should use the long form. Criteria for when a long form filing should be made are very broad. The choice of forms is important for merger parties because the ACCC has the discretion to prevent the clock from starting on its merger review if it considers that a notification is “materially incomplete”. We expect the ACCC will likely exercise this discretion if parties do not follow the ACCC’s guidance criteria for choosing the appropriate notification form.

Type of acquisition | Criteria for whether merger parties should use the long form | |

Horizontal acquisitions |

| |

Vertical acquisitions |

| |

Conglomerate acquisitions |

| |

Other circumstances |

|

The ACCC’s guidance asks merger parties to use the market definition that gives rise to the largest share (or the largest share increment, if different) based on the turnover, volume and/or capacity of the party to the acquisition. However, the ACCC emphasises that parties “do not need to accept that these are the most relevant or appropriate market shares for assessing the competitive effects of the acquisition” and “expects parties may consider alternative market definitions and market shares are more appropriate for assessing the acquisition”. Noting that it may be challenging to estimate market shares, the ACCC encourages parties to use their best efforts, provide the methodology for the calculations and not to select a methodology designed to produce the lowest shares or increment.

When do merger parties need to start using the new forms?

Any parties wishing to use the new notification process from 1 July 2025 (or are required to from 1 January 2026) will need to apply using the relevant short or long form. See our previous update regarding the availability of ACCC engagement options during 2025.

All acquisitions notified to the ACCC under the new merger process from 1 July 2025 will appear on the ACCC’s public register. However, the details of what will be published on this register has yet to be determined because there is currently a placeholder in the relevant part (Part 5) of the draft determination, which is due to commence from 1 July 2025.

Next steps

Submissions on the draft determination are due on 2 May 2025. The government will then consider the feedback before it finalises the determination ahead of the new notification regime becoming available for merger parties to use from 1 July 2025.

The government also indicated that the notification thresholds will be reviewed 12 months after coming into effect to assess whether they are working as intended.